Visão Geral: Os preços do laminado a frio em Xangai permaneceram estáveis de janeiro a fevereiro. Afetados pelo feriado do Ano Novo Chinês, a atividade geral do mercado não foi vibrante. No entanto, devido à pressão relativamente baixa de estoque, os comerciantes do mercado demonstraram forte intenção de manter as cotações firmes, mantendo os preços estáveis. Com o fim do feriado e a retomada gradual da produção pela manufatura downstream, como os preços do laminado a frio irão se comportar de fevereiro a março?

I. Revisão dos Preços do Laminado a Frio

Conforme mostrado no gráfico acima, os preços do laminado a frio se recuperaram e estabilizaram em níveis altos após flutuações em dezembro. O principal motivo foi o aumento de cerca de 5% na demanda aparente por produtos laminados a frio em dezembro de 2024 em relação ao ano anterior. Para enfrentar as políticas tarifárias previstas após a eleição de Trump, os setores de eletrodomésticos e automotivo aumentaram os pedidos de exportação urgentes, impulsionando a demanda por consumo de bobinas laminadas a frio. Em termos de oferta, embora a produção de bobinas laminadas a frio tenha permanecido superior ao mesmo período do ano passado, as condições climáticas afetaram a logística, desacelerando as chegadas gerais ao mercado. Isso levou a um leve descompasso entre oferta e demanda em dezembro, causando a recuperação e flutuação dos preços do laminado a frio. Entrando em janeiro, com os fabricantes de automóveis concluindo seus esforços de final de ano para atingir metas anuais e os pedidos de exportação urgentes terminando, a atividade do mercado esfriou gradualmente devido ao feriado do Ano Novo Chinês. No entanto, como as siderúrgicas mantiveram um forte sentimento otimista e os preços de liquidação permaneceram altos, juntamente com o acúmulo de estoque relativamente baixo após o feriado, a pressão de estoque foi relativamente pequena. Isso resultou na estabilização dos preços das bobinas laminadas a frio em níveis altos de janeiro a fevereiro.

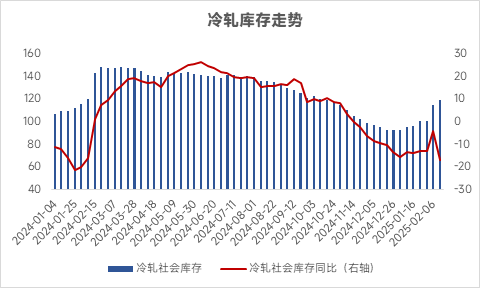

II. Estoque

Embora a baixa temporada e o feriado do Ano Novo Chinês tenham levado a um rápido acúmulo de estoque de produtos laminados a frio, o problema de acúmulo de estoque não foi significativo após o feriado. Especificamente, em 14 de fevereiro, o estoque social de laminados a frio apresentou uma queda anual de aproximadamente 16%. Atualmente, o estoque de laminados a frio continua a aumentar, com o pico e o ponto de inflexão ainda por aparecer. O pico de estoque é esperado para ocorrer por volta de meados de março.

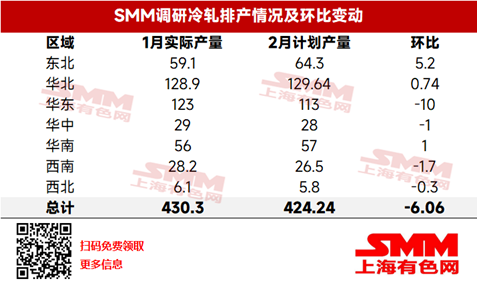

III. Oferta

Em termos de oferta de laminados a frio, de acordo com o último acompanhamento da SMM, a produção planejada de produtos comerciais laminados a frio de 31 siderúrgicas principais em fevereiro totalizou 4,242,400 toneladas, uma redução de 60,600 toneladas em relação à produção real de janeiro, uma queda de 1,4%. Em média diária, os dias mais curtos do calendário de fevereiro resultaram em uma produção planejada diária de 151,500 toneladas, um aumento de 9,2% em relação à produção média diária real de janeiro. No geral, a produção de laminados a frio em fevereiro permaneceu em níveis altos.

IV. Demanda

As bobinas laminadas a frio são consumidas principalmente nas indústrias automotiva, de eletrodomésticos e de fabricação de ferragens, com outros setores downstream representando uma proporção relativamente pequena do consumo total. Em termos de demanda, de acordo com o último relatório sobre os três principais eletrodomésticos da ChinaIOL, o cronograma total de produção de condicionadores de ar, refrigeradores e máquinas de lavar em fevereiro de 2025 atingiu 29,14 milhões de unidades, um aumento de 30,6% em relação ao ano anterior. Por produto, a produção de condicionadores de ar domésticos foi de 15,93 milhões de unidades, um aumento de 35,6% em relação ao ano anterior; a produção de refrigeradores foi de 6,32 milhões de unidades, um aumento de 29,2% em relação ao ano anterior; e a produção de máquinas de lavar foi de 6,89 milhões de unidades, uma queda de 21,3% em relação ao ano anterior. Em janeiro de 2025, a taxa de operação da indústria automotiva foi de 86,6%, um aumento de 6,9% em relação ao ano anterior. No entanto, o sentimento da indústria enfraqueceu este mês devido ao feriado do Ano Novo Chinês, com as empresas gradualmente interrompendo a produção no final do mês, desacelerando o ritmo de produção em todo o país. No entanto, algumas empresas relataram a continuidade da produção durante o feriado para atender pedidos acumulados. A SMM estima que a taxa de operação da indústria automotiva seja de 83,6% em fevereiro e 86,3% em março. No geral, a manufatura downstream está em um estado de recuperação gradual.

V. Conclusão

Para os preços do laminado a frio de fevereiro a março, o mercado atual está em um estado de equilíbrio apertado entre oferta e demanda, sem desequilíbrios significativos. Embora a pressão de oferta seja relativamente alta, levará tempo para que essa pressão seja transmitida ao mercado. Enquanto isso, a recuperação lenta da manufatura downstream e a falta de atividade vibrante no mercado também limitam o potencial de alta dos preços do laminado a frio. No geral, durante o acúmulo gradual do desequilíbrio entre oferta e demanda de fevereiro a março, espera-se que os preços ajustem-se em níveis altos. Estima-se que os preços de transação predominantes para produtos laminados a frio de 1,0 mm em Xangai variem entre 4,200-4,350 yuan/tonelada. No curto prazo, atenção deve ser dada a dois pontos: 1. A grande diferença de preço entre produtos laminados a quente e a frio e como ela se estreitará no futuro. 2. O impulso de reabastecimento pós-feriado no setor de manufatura, com monitoramento contínuo do estoque de laminados a frio.

![[SMM Steel Market Flash] POSCO visa retorno ao acionista de 35%-40% com base no lucro líquido ajustado](https://imgqn.smm.cn/usercenter/gmcdk20251217171720.jpg)

![[SMM Steel Market Flash] POSCO afirma que tensões no Oriente Médio continuam a comprimir margens do aço](https://imgqn.smm.cn/usercenter/zLhJl20251217171720.jpg)

![[Tema Quente SMM] Preços de BQL subiram em relação ao mês anterior em abril, expectativa de flutuação em níveis elevados antes de meados de maio](https://imgqn.smm.cn/usercenter/vhvTQ20251217171715.jpg)